Data Study on Student Loan Bonds

The skills the author demoed here can be learned through taking Data Science with Machine Learning bootcamp with NYC Data Science Academy.

Contributed by Zach Escalante. He is currently in the NYC Data Science Academy 12 week full time Data Science Bootcamp program taking place between April 11th to July 1st, 2016. This post is based on his second class project - R Shiny (due on the 4th week of the program).

Introduction:

Data shows Federal Family Education Loan![]() Program (FFELP) backed securities have long been viewed as a safe and steady fixed income cashflow with a AAA rating, appropriate for investors seeking principal preservation and predictable returns.

Program (FFELP) backed securities have long been viewed as a safe and steady fixed income cashflow with a AAA rating, appropriate for investors seeking principal preservation and predictable returns.

This changed on June 22, 2015 when Moody's rating agency placed $34 billion of these securities on downgrade watch (1). The rating agency Fitch soon followed suit, and by the fall of 2015 $71.2 billion FFELP backed loans were being reviewed for a potential ratings downgrade (2). The reason ratings agencies began to call into question the creditworthiness of these bonds (whose underlying assets are backed by the full faith and credit of the US Government) had to do with an expansion of Income Based Repayment (IBR) options to student loan borrowers by the White House in 2010 (3).

This provision enabled borrowers to maintain a 'current' status on their student loans by only paying a certain percentage of their disposable income towards their loan payment. In some cases, this amount does not cover the interest due on the loan (according to a fixed-rate-prepayment plan) causing potential cash shortfalls to the trust from which the securities are issued.

Since the borrower is not technically defaulting, the Federal Government is not obligated to fund the previously agreed-upon 97% of the unpaid principal and interest to the student loan trust in event of a default by the borrower, creating the possibility that certain FFELP backed bonds will not receive enough cashflow to adhere to their stated maturity date![]() .

.

Objective

During my time working on an Asset Backed Securities desk, investors frequently asked for various reports and spreadsheets to explain the underlying characteristics and potential for cash shortfalls of the FFELP bonds they were looking to add or sell in their portfolio. This gave me the idea to create a comprehensive and easy to access web application that provides the user with both time series and static quarterly data on the underlying assets in each bond.

Shiny Web Application Data:

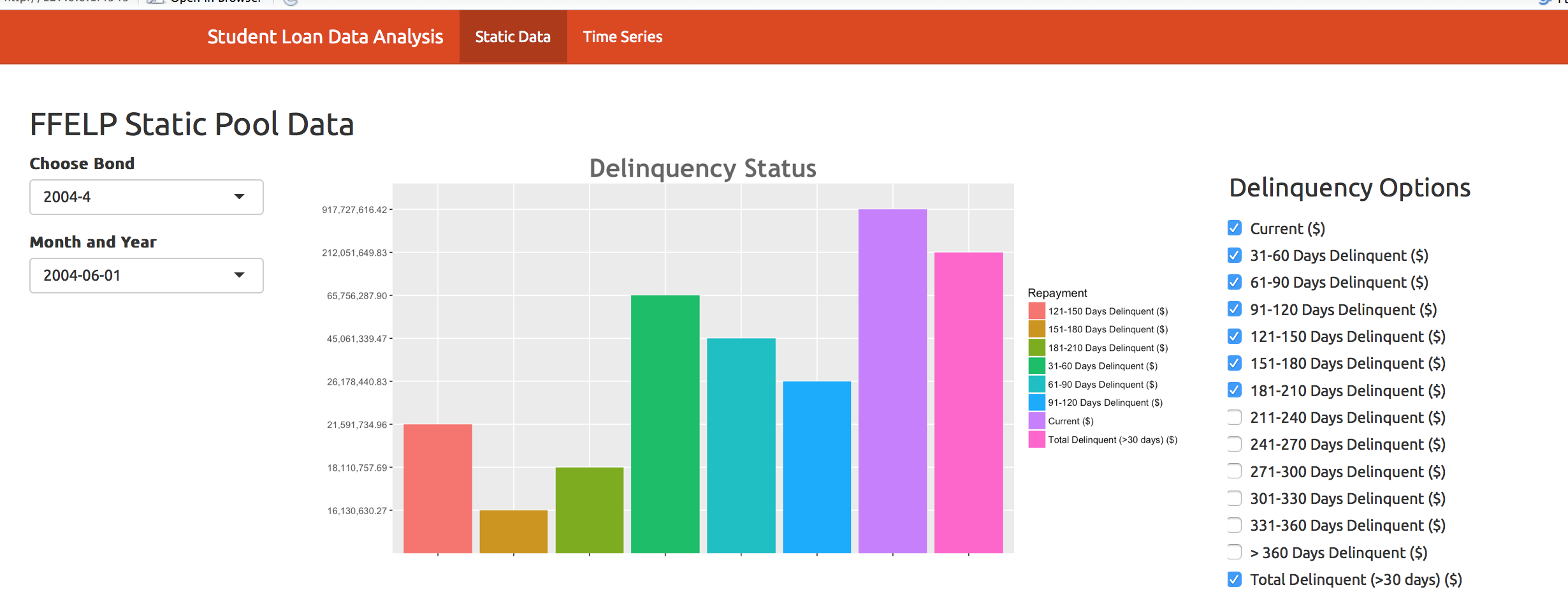

The dropdown menus underneath "FFELP Static Pool Data" allow the user to select both the bond and the quarter which they would like to evaluate (the list of bonds was obtained from the Navient website).

{kind=link}

The first chart shows us what amount of each delinquency status is present in the underlying loans of each bond, ranging from "Current", to ">360 Days" delinquent.

This provides valuable insight into what amount of the pool an investor might reasonably expect will enter default, and hence recoup 97% of their principal and unpaid interest from the Federal Government. We can also see what amount of the pool is not contributing cash to the trust, another potential source of delinquencies. Finally, historical delinquency data can also provide insight into the characteristics of borrower in the student loan![]() trust and how likely they are to re-finance their student loans into an Interest Based Repayment (IBR) plan.

trust and how likely they are to re-finance their student loans into an Interest Based Repayment (IBR) plan.

Repayment Status

The second chart on the page shows a repayment status snapshot for each bond. With this chart investors can see the amount of each loan trust that is still in school, forbearance, deferment, an IBR plan, and the total amount in repayment.

Loans with high IBR balances may have problems with generating the cashflow necessary to the student loan trust in order to pay off the trusts' liabilities (these are CUSIP'd securities) before their stated final maturity date

Loans with high IBR balances may have problems with generating the cashflow necessary to the student loan trust in order to pay off the trusts' liabilities (these are CUSIP'd securities) before their stated final maturity date![]() .

.

CPR

The next valuable aspect of this web application for analyzing bonds is time series data of prepayments (which can be found on the second tab). This is very important to decipher exactly how much of the loan pool has been paying off their student loans ahead of schedule. A significant drop in the Constant Prepayment Rate (CPR) could be another sign of potential trouble for the loan trust to adhere to its stated final maturity date![]() .

.

Future Improvements:

I believe this application is just the first step into financial education for investors without access to sophisticated software systems such as Bloomberg and Intex. Much of the data on the underlying assets of securitized products is obtainable, and with some re-formatting can be made easily readable as well.

The next stage of development of this application will include adding more tranches (such as consolidated student loan![]() pools) to the list of potential bonds for the investor to view. Also, I would like to add more time series data options for the user to be able to analyze on the second tab.

pools) to the list of potential bonds for the investor to view. Also, I would like to add more time series data options for the user to be able to analyze on the second tab.

To view the code for this project, please visit my Github account and click on the "ShinyApplication" link: https://github.com/zachescalante/Zach-Escalante-Code

Thank you for your interest in this web application. If you have questions comments, or additional suggestions for improvement, please feel free to reach me at zach.escalante@gmail.com

(1) https://www.moodys.com/research/Moodys-reviews-for-downgrade-106-tranches-from-57-FFELP-student--PR_328361

(2) https://www.bloomberg.com/news/articles/2015-12-23/after-math-error-fitch-doubles-student-debt-downgrade-estimate

(3) https://www.whitehouse.gov/issues/education/higher-education/ensuring-that-student-loans-are-affordable